By: Jason P. Huffman, CFP®, AAMS™, Financial Advisor

Data and policy actions cited are current as of May 13, 2026.

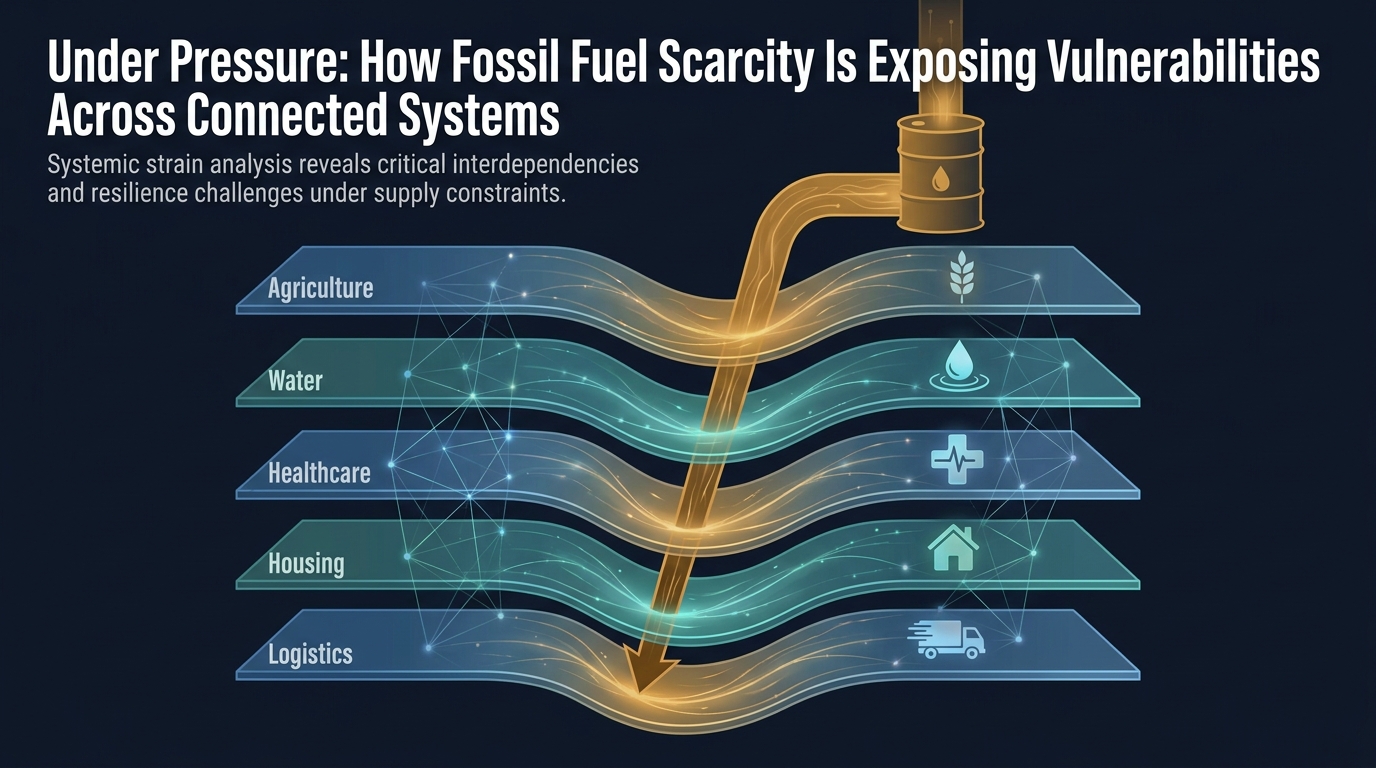

This is the third article in a four-part series analyzing the potential implications of the disruptions being created by the closing of the Strait of Hormuz. The first article established that fossil fuels are not just an energy source — they are a materials platform whose outputs are embedded across the economy. The second traced the allocation competition that emerges when that platform contracts — who gets the molecule, the barrel, the cylinder — and showed how pricing power, political visibility, and physical position determine which sectors are served first.

This article examines what happens downstream. The allocation decisions described in Article 2 do not stay in commodity markets. They transmit — through input costs, logistics costs, labor markets, and policy choices — into the sectors that feed, house, and provide healthcare to the population. The question is how far that transmission has traveled, how far it has yet to go, and what the aggregate data does and does not reveal about the answer.

Table of contents

Where the Data Stands

The Bureau of Labor Statistics released the April Consumer Price Index on May 12 and the April Producer Price Index on May 13. Together, they provide the first complete picture of consumer and wholesale price behavior across two full months of the Hormuz disruption.

The headline trajectory is clear. CPI inflation ran between 2.4% and 2.7% year-over-year from September 2025 through February 2026 — the six months preceding the crisis. In March, it jumped to 3.3%. In April, 3.8% — the highest since May 2023.[1]

The producer-level data moved faster. PPI final demand ran 1.8% to 3.8% year-over-year across the same pre-crisis window. In March, 4.0%. In April, 6.0% — the largest twelve-month increase since December 2022. The monthly gain of 1.4% was nearly triple the consensus forecast and the largest since March 2022.[2]

The gap between those two numbers is the forward-looking signal. PPI at 6.0% with CPI at 3.8% means roughly 220 basis points of producer-level cost pressure has not yet reached consumers. That pressure either compresses margins — which shows up as weaker earnings and reduced economic activity — or it passes through to consumer prices over the coming months. History suggests it passes through.

The sub-components show where the transmission is concentrated and where it has not yet arrived.

Energy is the primary vector, and it is not uniform. Fuel oil — which includes the diesel and heating oil that power freight, farming, construction, and backup generation — rose 54.3% year-over-year. Gasoline rose 28.4%. Electricity rose 6.1%, with EIA reporting average revenue per kilowatt-hour up 9% year-over-year in February, and sharper increases in data-center-heavy states: Virginia 26.3%, Ohio 21.9%, Pennsylvania 19.5%.[3] Natural gas rose only 3.0% — the one energy sub-component where U.S. domestic production provides meaningful insulation from the Strait disruption.

Food is early in the transmission cycle. Food at home rose 2.9% year-over-year — elevated but not yet reflecting the full cost structure of the 2026 growing season. Within that average, the distribution matters: fruits and vegetables rose 6.1%, the hottest food sub-category and the one most sensitive to diesel-driven transport costs on perishable supply chains. Beef rose 2.7% in April alone on a monthly basis, against a beef cattle herd at its smallest since 1951.[4] Dairy fell 0.6% year-over-year — the one declining category, reflecting a global oversupply cycle rather than cost insulation. Dairy producers are absorbing higher input costs into already-compressed margins; the dynamics behind that inversion are examined later in this article.[5]

The PPI detail reveals where pressure is building in the pipeline. Trade services margins — a measure of what wholesalers and retailers charge above their costs — surged 2.7% in a single month, the largest advance on record in data going back to 2010.[6] Truck transportation of freight rose 8.1% month-over-month. Stage 1 intermediate demand — the earliest inputs in the production chain — rose 8.9% year-over-year, the highest since October 2022. These are costs that have entered the system but have not yet exited through consumer prices.

Core CPI — which excludes food and energy — rose to 2.8%, up from 2.5% in February. Core PPI rose to 5.2%. The spread between core PPI and core CPI widened to 240 basis points. That spread is not energy-only. Services PPI rose 1.2% in April, the largest monthly gain since March 2022, with two-thirds of the increase in trade services.[6] The broadening into non-energy categories is the signal that distinguishes a transitory energy spike from a cost structure that is repricing across the economy.

None of this determines the outcome. It maps where the transmission has reached and where the lag remains. The sections that follow trace the specific channels — agriculture, water, healthcare, housing, logistics — through which these aggregate numbers connect to the sectors that serve households directly.

The Buffer

The disruptions documented in this series began in late February 2026. It is now mid-May. The reasonable question is: if these dependencies are as critical as described, why does daily life still feel approximately normal?

The short answer is buffers. The economy entered the disruption with inventories, reserves, contracts, and pre-purchased inputs that have been absorbing the shock. Some of those buffers remain. Others have been consumed.

On May 5, the oil tanker New Corolla docked at Long Beach, California, carrying 2 million barrels of crude oil — the last vessel to transit the Strait of Hormuz before the closure and the last shipment of Persian Gulf crude to reach the United States.[7] California receives roughly 30% of its foreign crude from the Gulf. Even if the Strait reopened tomorrow, refineries need weeks to process crude into finished products, and the logistics chain does not reassemble instantaneously. EIA’s May outlook assumes the Strait remains effectively closed through late May, with flows only slowly beginning to resume in late May or early June, and does not expect most pre-conflict production and trade patterns to normalize until late 2026 or early 2027.[8]

The drawdown is accelerating. Morgan Stanley estimates that global oil stockpiles fell by approximately 4.8 million barrels per day between March 1 and April 25 — exceeding any previous quarterly drawdown in International Energy Agency data.[9] U.S. gasoline inventories stood at 222 million barrels as of late April, the lowest for that time of year since 2014 and more than 2 million barrels below the five-year seasonal average. Morgan Stanley’s base case projects inventories falling below 200 million barrels by the end of August — lower than any level for that period in modern data — driven by a collapse in East Coast gasoline imports from Europe and the Middle East, a refinery shift toward diesel and jet fuel production at gasoline’s expense, and elevated U.S. exports as foreign buyers compete for available supply.[10] U.S. distillate stockpiles — the diesel and heating oil that power freight, farming, and construction — were at their lowest point since 2005.[9] Governments have responded with a coordinated IEA release of 400 million barrels from emergency strategic reserves — the largest such deployment on record.[11]

The refinery dynamic deserves attention because it illustrates the allocation competition described in the second article of this series. Refiners are not reducing output. They are shifting their product slate — producing more diesel and jet fuel, where margins are highest, and less gasoline, where consumer demand is most visible. That is an economically rational response to scarcity pricing. It also means that the consumer fuel most Americans interact with daily is being deprioritized relative to commercial and industrial fuels. The allocation hierarchy is not abstract. It is operating inside the refinery.

Helium’s buffer was shorter. Cryogenic helium containers must reach their destination within approximately 45 days of liquefaction before the helium warms and escapes. AP reports that about 200 specialized containers were stuck in the Middle East when the Strait closed.[12] The 45-day window has expired. The helium inside those containers has vented — not delayed, but permanently lost. SEMI, the semiconductor industry association, estimates that even if the Strait opened today, it would take four to six months to normalize helium supply.[13]

The agricultural buffer is the longest and the most important for household costs. The 2025 harvest — planted and grown before any of these disruptions — is still flowing through the food supply chain. Grocery shelves are stocked with food produced under the old cost structure. The 2026 crop is being planted now, under the cost conditions described in the next section. The gap between what consumers are paying today and what the current production economics require will narrow over the coming months as the 2025 supply is consumed and 2026 production — grown with more expensive fertilizer, more expensive diesel, and in some regions less water — replaces it. The April CPI food data confirms this timing: food at home at 2.9% year-over-year does not yet reflect the fertilizer price shock that arrived after most spring inputs were pre-purchased.[4]

One additional gap runs through every cost figure in this article and the series. The oil prices reported in financial media — Brent futures, West Texas Intermediate — are prices for contracts to deliver oil in the future. The price for physical barrels available for immediate delivery is materially higher. In April 2026, dated Brent — the price for actual cargoes loading within weeks — reached $132 to $144 per barrel, while Brent futures for the same period traded at $96 to $100. S&P Global Platts reported that Saudi Arabia raised its official selling price for Arab Light to a premium of $19.50 over its benchmark — a level that had never previously exceeded $10.[14] The diesel, gasoline, jet fuel, and fertilizer costs cited throughout this series are ultimately determined by physical delivery prices, not futures. The cost figures in this article are likely understated relative to what refiners, distributors, and end users actually pay.

The lag between disruption and felt impact is real. It is not evidence that the transmission has stopped. It is evidence that buffers have been doing their job. The question — which the rest of this article examines sector by sector — is what happens as those buffers thin.

The Farm Crisis

The agricultural sector entered 2026 already under financial stress. The Hormuz disruption did not create the farm crisis. It arrived on top of one.

Chapter 12 family farm bankruptcies surged 46% in 2025, reaching 315 filings — the second consecutive year of significant increases.[15] The American Farm Bureau Federation projects total farm debt will reach a record $624.7 billion in 2026, with interest expenses hitting a record $33 billion.[16] USDA’s Economic Research Service forecasts roughly $44 billion in net cash income losses across nine major crops for the 2025–2026 cycle.[17] A Purdue University Center for Commercial Agriculture survey of 400 farmers conducted in late March 2026 found that nearly half said their operation is financially worse off than it was a year ago.[18]

The underlying dynamic is a margin squeeze: input costs are historically elevated while commodity revenues have declined. Corn has fallen from approximately $7 per bushel at its 2022 peak to roughly $4.50 — against a breakeven of $5.00 to $6.00 per bushel depending on soil productivity and cost structure.[19] Soybean farmers lost an estimated $89 per planted acre on their 2025 crop — the third consecutive year of market losses.[20] Global soybean production has set consecutive records, driven primarily by Brazil. U.S. soybean exports to China remain 15–20% below historical norms — a consequence of retaliatory tariffs that accelerated China’s shift toward Brazilian suppliers, a trend that predated the current tariff regime but has been substantially worsened by it.[21]

That was the baseline. Then fertilizer and diesel prices spiked.

What the Hormuz disruption added

University of Illinois farmdoc daily reports that in the six weeks following the Hormuz closure, urea prices surged 49%, UAN jumped 38%, and anhydrous ammonia climbed 32%.[22] BLS data updated this picture further: as of April 17, anhydrous ammonia stood at $1,123 per ton, urea at approximately $826 per ton (up 35%), and 28% UAN solution at $543 per ton — translating to roughly $20–23 per acre in additional cost on corn alone.[23] Diesel — which powers every tractor, combine, irrigation pump, grain dryer, and truck on a farm — rose 54.3% year-over-year through April in the BLS fuel oil index.[24]

On a mid-size Midwest corn and soybean operation — 1,500 acres, a realistic family farm — the fertilizer spike adds $60,000 to $90,000 in costs in a single season. The diesel increase adds at least another $10,000. For irrigated Southern operations the numbers are worse: a Mississippi rice farmer’s fuel costs now run approximately $150 per acre, meaning a 1,500-acre rice operation faces $225,000 in fuel alone — before accounting for the diesel consumed by irrigation pumps, which on many Southern farms are the single largest fuel expense.[25]

Tariffs compound the energy-driven cost increase. A $100-per-ton tariff-related increase in fertilizer costs, applied across 1,500 acres at typical nitrogen application rates, adds $10,000 to $15,000 — layered on top of the war-driven spike. Steel tariffs at 50% raise the cost of replacement parts for tractors, combines, planters, and grain bins.[26]

The April CPI data confirms that these costs have not yet fully reached consumers. Food at home rose 2.9% year-over-year — elevated but moderate. That number reflects the 2025 harvest, produced under the old cost structure. Most spring 2026 fertilizer was pre-purchased at lower prices. The full nitrogen cost shock hits fall 2026 applications and shows in 2027 food prices. Current food CPI understates the forward trajectory.[24]

Why farmers cannot pass costs through

The natural question is: if input costs rise and supply falls, why don’t crop prices rise to compensate?

The answer lies in the structure of agricultural markets. A farmer is a price taker, not a price setter. A farmer plants in April based on projected costs and a harvest price that the global commodity market will determine five to six months later. When a Kansas wheat farmer’s input costs spike because of U.S. tariffs on fertilizer, the global price of wheat does not move in response — because Brazil, Australia, Argentina, and Russia are still producing at their own cost structures. The American farmer’s margins compress even as global supply tightens, because the price signal takes months to propagate and competing producers partially fill the gap.

Many farmers compound this by selling forward — locking in harvest prices months before planting to manage risk. If input costs spike after they have locked their selling price, they are trapped in a margin that no longer works. And the farmer captures roughly 14 to 16 cents of every dollar spent on food at retail. The rest goes to processing, packaging, transportation, and retail. When costs rise across the entire chain, each intermediary protects its own margin, and the farmer — who has the least pricing power of any participant — absorbs the most compression.

Why this reaches every aisle in the grocery store

The reason the farm crisis is a food price crisis — not just a farmer crisis — lies in what corn and soybeans actually become after they leave the farm.

Roughly 36% of U.S. corn production goes to animal feed — the primary caloric input for cattle feedlots, hog operations, poultry houses, and dairy. When corn input costs spike, the cost of producing every major animal protein spikes with it. Another roughly 34% goes to ethanol production, which means corn competes with fuel demand for the same acres — and ethanol costs flow directly into gasoline blending. The remainder enters the food processing chain as corn syrup, corn starch, and corn oil. Soybeans follow the same pattern: soybean meal is the other half of the animal feed ration, and soybean oil is one of the most widely used cooking and food processing oils in the United States.[27]

The April CPI sub-components show the early stages of this transmission. Beef rose 2.7% in a single month, against a beef cattle herd at its smallest since 1951. Fruits and vegetables rose 6.1% year-over-year — the hottest food sub-category, and the one most sensitive to diesel-driven transport costs on perishable supply chains. Nonalcoholic beverages rose 5.1%, reflecting multi-year coffee commodity price increases now compounding with shipping and energy costs.[24]

Economists typically argue that when one protein becomes expensive, consumers substitute — beef gets expensive, buy chicken. Under normal conditions, where one commodity is stressed in isolation while alternatives remain cheap, this is true. Under the current conditions, the substitution model is impaired. Beef, chicken, pork, eggs, and grain-based products are all experiencing input cost pressure simultaneously, because they share the same corn and soybean feed base, the same diesel-dependent logistics, the same petrochemical-derived packaging, and the same fertilizer supply chain that traces back to the natural gas platform described in the first article of this series.

That is the inflationary transmission mechanism: supply-driven cost increases propagate from energy through fertilizer through farming through feed through protein through retail, arriving at the consumer’s grocery bill as broad-based food price inflation — after they have already compressed farm margins along the way. The PPI data confirms the pipeline is loaded: producer prices for processed foods for intermediate demand rose 6.6% year-over-year in March, with stage 1 intermediate demand at 8.9% in April.[28] Those are costs that have entered the production chain but have not yet exited through consumer prices.

The policy mismatch

Federal support infrastructure was not designed for the kind of stress that arrived. The farm bill that governs agricultural policy expired in 2023 and has not been replaced. In January 2025, the administration froze $19.5 billion in IRA-funded conservation program payments — money allocated to farmers who had already signed binding contracts with USDA. A federal judge ordered the funds released; USDA released $20 million of the billions owed. More than $6 billion in contracted farmer investments were frozen or canceled.[29]

The One Big Beautiful Bill Act, signed in July 2025, contains meaningful agricultural provisions — reference prices raised 10–21% for major commodities, 30 million new base acres added to ARC/PLC eligibility. But those provisions are structurally mismatched to the current crisis in timing and mechanism. Tax deductions help profitable farms, not farms that are cash-negative because input costs exceed revenue. Price floors protect against commodity price collapse, but the problem in 2026 is that costs are too high for any price to cover. Implementation lag compounds the mismatch: even provisions that could help require months of USDA rulemaking and enrollment before cash reaches a farmer.[30]

Direct government payments provide the most immediate buffer. Farm payments are forecast at $44.3 billion for 2026 — a $13.8 billion increase from 2025. The Farmer Bridge Assistance Program is providing $12 billion in one-time direct payments, with nearly $9.6 billion disbursed to approximately 500,000 farms by early April.[31] On the 1,500-acre example operation, bridge payments total roughly $56,000 — which does not cover the full fertilizer and diesel cost increase of $70,000 to $100,000, but covers more than half of it, and arrives as direct cash during planting season. Whether that buffer is sufficient depends on how long the cost pressure persists and whether commodity prices recover. The OBBBA’s permanent safety net improvements begin triggering after October 1, 2026.[32]

The Water Constraint

The farm crisis documented in the previous section assumes water is available. In substantial parts of the western United States, that assumption is under stress.

Eight western states — Arizona, Colorado, Idaho, Nevada, New Mexico, Oregon, Utah, and Wyoming — recorded their lowest April 1 snow water equivalent values since SNOTEL monitoring began in the 1980s. California recorded its second-lowest. The January-through-March period of 2026 was the driest such stretch on record for the contiguous United States. Colorado’s snowpack peaked a full month early — March 8 instead of the typical April 8 — after the state recorded its warmest March, with temperatures nearly 14 degrees above normal.[33]

The Colorado River system, which supplies water to more than 40 million people across seven states, has dropped to approximately 36% of storage capacity. Lake Powell stood at 24% as of mid-April, approaching the minimum elevation required to generate hydroelectric power. The Bureau of Reclamation responded with emergency releases from the upstream Flaming Gorge Reservoir into Lake Powell while simultaneously reducing releases from Powell to Lake Mead — cuts from 7.5 million acre-feet to 6 million acre-feet annually. Upper Basin inflow is forecast at 23% of normal. The Bureau projects these measures could reduce Hoover Dam’s hydroelectric generating capacity by 40% by fall 2026.[34]

That hydroelectric loss connects directly to the energy cost structure. Reduced generation at Hoover Dam and Glen Canyon Dam means electricity must be sourced from alternative generators — primarily natural gas — at a time when natural gas prices are elevated by the Hormuz disruption. The grid that serves the Southwest must burn more expensive fuel to replace the hydroelectric power lost to drought. The April CPI showed electricity up 6.1% year-over-year nationally, but the regional figures in drought-affected states with hydroelectric dependence are higher and accelerating.[24]

The Colorado River’s operating agreements expire at the end of 2026. The seven basin states have not agreed on new rules for sharing water. A February deadline was missed. States are now publicly discussing litigation. If no agreement is reached, the federal government may impose allocation decisions — a scenario with no modern precedent for a resource of this scale.[35]

For agriculture, the implications are direct. The Colorado River Basin supports some of the most productive farmland in the country, including California’s Imperial Valley — which produces a significant share of the nation’s winter vegetables — and Arizona’s agricultural sector. Water restrictions are already forcing cuts to agricultural allocation. Those cuts layer onto the input cost increases documented in the previous section: the same farms facing higher fertilizer and diesel costs are, in irrigated western regions, also facing reduced water availability. The fruit and vegetable sub-category showing 6.1% year-over-year inflation in April CPI is disproportionately sourced from these regions.[36]

Corpus Christi: Where Water Meets Energy

The intersection of water scarcity and fossil fuel infrastructure reaches its most acute expression in Corpus Christi, Texas — the nation’s top crude oil export hub and a major petrochemical manufacturing center.

The city’s two primary reservoirs — Lake Corpus Christi and Choke Canyon — stood at a combined 8% of capacity as of early May 2026, with Choke Canyon at 7.4% and Lake Corpus Christi at 11.2%. Choke Canyon fell from 47% to below 8% between October 2021 and early 2026 — the physical signature of a five-year drought, with year-to-date rainfall at less than 60% of normal. Lake Corpus Christi has reached its lowest level since the reservoir was created in 1958. The city’s water supply models have converged on a single projection: Level 1 Water Emergency by September 2026 — triggered when the city is 180 days from the point at which total water supply can no longer meet total water demand.[37]

The city is under Stage 3 water restrictions, requiring a 15% reduction in citywide use. Residents have not been allowed to water lawns since 2023. City data show roughly 70% of homes already use less water than the restrictions require — the residential population has been squeezed for essentially all it can give.[38]

What makes Corpus Christi structurally significant — rather than a regional drought story — is that the same water system serving 500,000 residents also supplies one of the nation’s leading petrochemical and refining complexes. The port injected more than $113 billion into the Texas economy in 2024 and supports more than 864,000 jobs nationwide. Industrial users collectively consume roughly half the region’s water. In December 2025, Moody’s downgraded the city from Aa2 to A1 and its utility revenue bond rating from Aa3 to A1, citing water supply risk — a credit downgrade driven by drought, not fiscal mismanagement.[39]

The industrial water consumption reflects decisions made over the preceding 15 years. The Gulf Coast Growth Ventures plastics plant — a $7 billion joint venture between ExxonMobil and Saudi Basic Industries Corp. that began operations in 2022 — uses approximately 13 million gallons of water per day, roughly 13% of the city’s entire supply. This facility came online during the drought. In the years preceding the crisis, the region welcomed major petrochemical plants from Exxon and Occidental Chemical, along with expansions at Valero and Flint Hills refineries. No commensurate water supply was developed. A desalination plant discussed for over a decade was canceled by the city council in September 2025, then reversed — the city has since included desalination in a broader infrastructure plan alongside emergency groundwater wells and reclaimed water systems. The former CEO of the city’s water utility put it directly: “We did not simultaneously add new water supply. We thought everything was going to be OK. But it was not going to be OK. And we should have known better.”[40]

The city council is weighing a mandatory 25% water curtailment across all customer classes — five times the 5% reduction originally specified in the contingency plan for a Level 1 emergency. A spokesperson for Flint Hills Resources, which supplies jet fuel to Texas airports from its Corpus Christi refinery, warned at a city council meeting that mandatory cuts “would force the shutdown of at least some aspects of our operations.” Enforcement faces a structural complication: approximately eight major industrial customers, including Valero, Citgo, and Flint Hills, enrolled years ago in a drought surcharge exemption program, paying an additional 31 cents per 1,000 gallons in exchange for permanent exemption from drought surcharges. Those users must still comply with mandatory curtailment, but the surcharge is the city’s primary financial penalty for noncompliance. Without it, enforcement requires individual citations through the court system, with water shutoff authority available only after two convictions.[41]

This is a fossil fuel supply constraint caused by water, not geopolitics. Corpus Christi’s refineries and petrochemical plants produce jet fuel, gasoline, diesel, plastics, and chemical feedstocks that enter national supply chains. If mandatory water curtailment forces partial shutdowns, the production loss compounds the supply constraints already caused by the Hormuz closure — a second independent vector of energy supply disruption, entirely domestic and entirely unrelated to war. Whether it materializes depends on rainfall, curtailment enforcement, and the pace of emergency infrastructure. The September 2026 projection is the city’s own modeling, not a worst case imposed from outside.

The Logistics Chain

The cost increases documented in the preceding sections — fertilizer, diesel, water — do not arrive at the consumer directly. They travel through a logistics system that adds its own costs at every stage. In May 2026, every major transportation mode that moves agricultural products, energy, and goods across the United States is degraded simultaneously. The degradation in each mode is compounding the others, because when one mode fails, the overflow shifts to alternatives that are themselves already under stress.

The refinery tradeoff

The closure of the Strait of Hormuz removed approximately 20% of global oil transit and the largest single source of jet fuel supply to the global market. The downstream effects illustrate the co-product constraint described in Article 1.

Europe imported the majority of its jet fuel from Middle Eastern refineries. With that supply cut, Lufthansa eliminated 20,000 short-haul flights through October. Turkish Airlines stopped serving 23 cities. United Airlines cut 5% of its summer schedule. European jet fuel prices doubled year-over-year to $187 per barrel.[42] American refineries responded by producing more jet fuel and diesel for export — but a refinery cannot produce more of one product without producing less of another. California refineries boosted jet fuel output by 20,000 barrels per day and diesel by 16,000 barrels per day while cutting gasoline output by 32,000 barrels per day. The result, reported by CNN, was a gasoline inventory draw of 6.1 million barrels in a single week, wholesale prices up 74 cents, and retail prices up more than 30 cents per gallon — the fastest increase since the war began.[43]

This is the allocation competition from Article 2 expressed inside the refinery. Diesel and jet fuel command substantially higher margins than gasoline — the Dallas Fed’s March Energy Indicators report shows refinery crack spreads rose 176% from the start of the year, with distillate margins at their highest since 2022.[44] Refiners followed the margin, and the American consumer’s gasoline supply became the residual claimant. The EIA projects U.S. jet fuel days of supply will fall to 21 days in 2026 — the lowest since 1963. Combined inventories of gasoline, diesel, and jet fuel are forecast to reach their lowest levels since 2000.[45]

The jet fuel constraint reaches beyond airlines into supply chains most people do not associate with aviation. Air freight carries a disproportionate share of high-value, time-sensitive goods — fresh produce, pharmaceuticals, vaccines, blood products, and transplant organs. When airlines cut routes and raise fuel surcharges, air freight capacity contracts with it. Perishable goods requiring cold-chain integrity face longer transit times, fewer routing options, and higher costs. The gap on the grocery shelf is not always filled.

The Mississippi River

The most cost-effective way to move grain from the Midwest to export terminals is by barge down the Mississippi River system. Close to half of all U.S. corn, soybean, and wheat exports travel this route — approximately 65 million metric tons per year in normal conditions. The efficiency is significant: a single barge carries roughly 1,750 tons of grain. A standard 15-barge tow moves as much as two 100-car unit trains or approximately 1,000 semi-trucks. Barge transport costs roughly one-tenth of rail and one-sixteenth of trucking per ton-mile.[46]

For the fourth consecutive year, the river is not running normally.

Persistent drought has reduced water levels to near-record lows. The river at St. Louis dropped more than 22 feet between midsummer and fall 2025. Levels near Memphis approached negative 5.5 feet on the gauge. When water levels drop, barges carry lighter loads — every foot of reduced depth means approximately 7,000 fewer bushels of soybeans per barge. Overall load reductions range from 10 to 15% in moderate conditions to 30 to 40% in severe drought. Tow sizes are reduced by up to 34%.[47]

Southbound grain shipments plunged roughly 79% from early harvest levels in fall 2025. Soybean movement fell nearly 90%. Barge freight rates at St. Louis surged to over 900% of the underlying tariff benchmark — compared to a non-drought average of roughly 350%. Cairo-Memphis shipments averaged $18.84 per ton versus $14.03 in non-drought years.[48] Higher barge freight rates weaken the cash basis for grain at river terminals, further squeezing margins for the same farmers already absorbing fertilizer, diesel, and tariff cost increases. An Iowa State agricultural economist described it as “a double whammy — they’re facing lower prices for their corn and soybeans if we can’t move as fast down the river, but we’re also facing higher fertilizer, higher input costs because of that same problem.”[49]

Rail

Rail grain carloads surged 16.9% year-to-date through Q1 2026, leading all commodity categories. Weekly Class I grain originations ran 10% above prior year and 6% above the three-year average. The overflow from the river is moving. The system is functional.[50]

The cost of that absorption is significant. During the fall 2025 barge crisis, shuttle secondary railcar bids surged to $563 above the underlying tariff — an increase of $138 in a single week. For grain that would have moved by barge at $14 to $26 per ton, the shift to rail at those premiums represents a cost multiple that flows directly to the farmer.[51]

The system also has less surge capacity than it did a decade ago. Class I railroads cut their workforce from 210,000 in 2015 to 149,000 by 2023 — a 29% reduction — as the industry adopted precision-scheduled railroading, a strategy that optimizes train length and scheduling to maximize operating ratios. The system runs more efficiently under normal conditions, but the buffer capacity that would allow it to absorb a sustained barge-to-rail shift was optimized away. The 2022 Mississippi drought forced a similar overflow and produced compounding congestion serious enough that the Biden administration intervened to prevent a simultaneous rail labor strike from shutting the network down.[52]

Rail equipment is not reserved for grain. In Q1 2026, petroleum and petroleum product carloads were up 7.7% and chemicals up 3.8% — other commodities competing for the same capacity, some driven by the same Hormuz disruption stressing the barge system. And rail runs on diesel. Every diesel cost increase documented in this article applies to rail operations. Rail is four times more fuel-efficient than trucking per ton-mile, but the fuel oil price increase of 54.3% year-over-year raises rail operating costs, which flow into railcar rates, which flow into farmer margins.[53]

Trucking

Every product that reaches its final destination in the United States travels by truck for at least the last mile. The BLS fuel oil index — up 54.3% year-over-year — flows directly into freight rates for every consumer good, agricultural input, construction material, and medical supply.

The cost does not hit all operators equally, and the structural difference matters. Large carriers — J.B. Hunt, Knight-Swift, Schneider — operate under long-term contracts with fuel surcharge clauses that adjust automatically. They run more efficient fleets and have access to hedging. The cost passes through their contracts.[54]

Small fleet owners and independent owner-operators are in a different position. They negotiate spot market rates without a fuel carveout. A principal analyst at DAT Freight & Analytics put it directly: small operators on the spot market are “lucky to recover half of higher fuel costs in their rates.” These operators handle a disproportionate share of spot freight and agricultural first-mile logistics. They entered 2026 already fragile — the post-pandemic capacity cycle of 2021–2022 drew in a surge of new operators chasing high rates, demand slipped, and the industry spent three years with too many trucks chasing too little freight. Thousands exited. The diesel spike arrived just as survivors were beginning to see recovery. If sustained prices force more small operators to park rigs or go bankrupt, that tightens capacity and raises rates for whatever freight remains — a self-reinforcing cycle in which the cost ultimately reaches the farmer shipping grain and the consumer buying groceries.[55]

The PPI data confirms this transmission is underway. Truck transportation of freight rose 8.1% month-over-month in April — the largest single-month gain in the PPI trucking index since 2022. That cost is embedded in the price of everything that travels by road.[28]

The workforce constraint across sectors

One additional pressure is operating across agriculture, construction, and trucking simultaneously, though it is typically analyzed in each sector separately.

In February 2026, the Federal Motor Carrier Safety Administration issued a final rule limiting non-domiciled commercial driver’s license eligibility to a narrow set of visa categories. FMCSA estimates the rule will reduce non-domiciled CDL holders from approximately 200,000 to 6,000 over the next several years. Industry analysis suggests the actual impact could reach 214,000 to 437,000 when combined with English language proficiency enforcement. In California alone, approximately 13,000 non-domiciled CDLs were canceled on a single day in March. The rule survived legal challenge in May when a federal appeals court denied a petition to pause it.[56]

The CDL rule arrives against a labor market that was already tightening — the trucking industry entered its first driver shortage in four years in early 2026, with more than 22 million Baby Boomers reaching retirement age by 2030 and a projected net driver shortage of approximately 292,000 by 2028, before accounting for the regulatory removal.[57]

This is not an isolated trucking story. Immigrants make up 34% of the agricultural workforce, 34% of the construction workforce nationally — exceeding 60% in specialties like drywall, roofing, and plastering — and a substantial share of CDL holders now subject to the FMCSA rule. Three sectors documented in this article — agriculture, housing construction, and freight transportation — share overlapping labor pools that are being reduced by the same policy direction at the same time. The result is fewer workers growing food that costs more to produce, fewer workers building housing that costs more to construct, and fewer drivers available to move either — at diesel prices 54% higher than before the war.[58]

Ukraine’s parallel supply pressure

The Hormuz closure dominates the energy story, but a second, independent supply-side disruption is operating concurrently. Bloomberg data compiled through April show Ukrainian strikes on Russian oil infrastructure reached a four-month high, including at least 21 attacks on refineries, pipelines, and offshore assets in April alone — part of a campaign that hit Russian energy facilities approximately 120 times in 2025. By April, Russia’s average refinery throughput had dropped to 4.69 million barrels per day, the lowest level since December 2009. The Tuapse refinery — one of Russia’s ten largest — has been offline since April 16. Nine Russian refineries suspended operations during the spring of 2026.[59]

Ukraine has escalated beyond refineries to Russia’s two largest Baltic Sea export terminals at Primorsk and Ust-Luga, which together handle roughly two-fifths of Russia’s seaborne oil exports. The Russian economic research center CMAKP estimates that export capacity fell by approximately 1 million barrels per day — roughly 20% — as a result of the strikes on port infrastructure. CMAKP nearly halved its 2026 Russian GDP growth forecast in response.[60]

This matters because even if the Iran situation resolves — even if a deal closes tomorrow — the Ukraine vector persists independently. Russian refining capacity does not rebuild overnight. Shadow fleet vessels that have been struck do not return to service. The supply-side pressure on global energy markets has two independent sources, and resolving one does not resolve the other.

Healthcare

The healthcare system is experiencing a version of the same structural pattern documented in agriculture and logistics: multiple independent cost pressures arriving simultaneously at institutions with minimal financial reserves.

The first two articles in this series documented healthcare’s material dependencies. IV bags, syringes, surgical devices, and the ethylene oxide sterilization process that makes 20 billion medical devices safe to use annually all trace back to the petrochemical platform now under supply stress. The helium shortage threatens the MRI systems on which 95% of diagnostic imaging depends. In both cases, healthcare competes for constrained supply against sectors with deeper margins — semiconductor manufacturers outbid hospitals for helium, and industrial-grade polymer demand crowds out the medical-grade resins that carry lower margins. The Baxter IV fluid crisis of 2024–2025, when a single flooded plant collapsed 60% of national IV supply for ten months, demonstrated the fragility at a single point. The current contraction is broader.[61]

The pharmaceutical supply chain adds a direct transmission channel between the Hormuz disruption and the medicine cabinet. The United States sources roughly 47% of its generic prescriptions by volume from India. India depends on the Strait of Hormuz for approximately 40% of its crude oil imports — oil that feeds the petrochemical inputs used throughout pharmaceutical manufacturing. Chemical inputs produced in China are commonly consolidated through Gulf logistics hubs in Dubai and across the UAE before shipment to Indian manufacturers. The connection runs in both directions: India needs the Strait to receive manufacturing inputs and to ship finished medicines west.[62] The Council on Foreign Relations reported that commercial activity through the Strait remained 90% below pre-war levels as of mid-March, while global air-cargo capacity dropped 79% in the Gulf region in the first days of the conflict, driving a 22% reduction worldwide. The GCC region — Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE — serves as a pharmaceutical transit hub worth $23.7 billion, approximately 80% of which relies on imports through GCC airspace and the Strait.[63]

The vulnerability was structural before the crisis arrived. An AMA survey of 902 primary care physicians, published in JAMA Network Open in January 2026, found that 88% had experienced drug shortages in the preceding six months — with one in five patients affected. Eighty-seven percent reported that shortages negatively affected care quality, with 92% forced to alter the drug of choice and 63% postponing prescribing. The drug categories with the highest rates of severe outcomes were endocrinologic drugs, stimulants, and infectious disease treatments.[64] A separate analysis in JAMA Health Forum found that 33.7% of generic active pharmaceutical ingredients for the U.S. market were produced by a single facility, and another 30.4% by only two or three facilities — a degree of concentration that makes the supply chain vulnerable to any single-point disruption.[65] The U.S. Pharmacopeia conducted a vulnerability assessment finding that as of February 2026, 30 of the 100 drugs it identified as highest-risk were already in active FDA shortage. The remaining 70 were flagged not because they are in crisis today but because the architecture of their supply chains makes them candidates for one.[66]

The cost transmission is now measurable at the source. Indian pharmaceutical industry associations report that active ingredient and intermediate prices have surged 50 to 180%, with air freight charges doubling and sea route surcharges increasing $4,000 to $8,000 per cargo. The Indian government implemented a three-month customs duty exemption on certain petrochemical products through June 30 in an attempt to stabilize pharmaceutical input costs.[67] Generic drugs operate on the thinnest margins of any pharmaceutical category. A Council on Foreign Relations senior fellow observed that when input costs rise, the effect on an inexpensive generic is proportionally far greater than on a branded drug costing $1,000 per treatment course.[63] That margin structure creates a specific risk: if costs rise enough, manufacturers may exit the market entirely rather than produce at a loss — a dynamic one industry expert described as a potential “force majeure reason to get out of contracts and leave the marketplace for something that already isn’t really viable.”[68]

The disruption is global and it is already producing measurable effects outside the United States. In the United Kingdom, generic manufacturers representing 85% of NHS prescriptions reported receiving only a quarter of their usual supply volume of critical chemicals since the war began. NHS England’s chief executive warned that certain medical supplies could run out within days. The cost of aspirin — a petrochemical derivative — spiked more than 1,000% at some UK pharmacies during the shortage.[69] India supplies generics to more than 200 countries; supply chain disruptions affecting Indian pharmaceutical exports threaten affordable medicine access across Africa, Southeast Asia, and the Middle East — regions where Indian generics are often the only affordable treatment option.[63]

The April CPI data shows medical care prices actually fell 0.1% month-over-month — one of the few deflationary pockets in the current data. That figure is misleading as a forward indicator. CPI medical care reflects administered prices (insurance premiums, negotiated reimbursement rates) that adjust on annual cycles, not spot market dynamics. The input costs that hospitals and providers are absorbing now — higher petrochemical-derived supply costs, higher energy costs for facility operations, higher logistics costs for pharmaceutical and device delivery, and the pharmaceutical supply chain pressures documented above — will show up in CPI medical care with a lag of six to eighteen months, as contracts reprice and insurers adjust premiums.[24]

Layered onto rising input costs is fiscal contraction. The One Big Beautiful Bill Act cuts federal Medicaid spending by approximately $911 billion over the next decade, according to CBO estimates, and is projected to increase the number of uninsured Americans by 10 million by 2034. Because the OBBBA is projected to increase the deficit, CBO projects it would trigger approximately $500 billion in additional mandatory Medicare spending reductions between 2026 and 2034, including a 4% reduction in hospital payments — unless Congress acts to circumvent them.[70]

These cuts fall disproportionately on the institutions with the least capacity to absorb them. Rural hospitals operate with an average margin of 3.1%, with 44% already running negative margins. The Chartis Center for Rural Health classifies 734 rural facilities — roughly one in three — as financially at risk. Since 2005, 193 rural hospitals have closed, with the pace accelerating. The OBBBA includes a $50 billion Rural Health Transformation Fund, roughly $10 billion per year against $911 billion in Medicaid cuts over the same period.[71]

The OBBBA also restructures the provider tax rules that nearly every state uses to finance its share of Medicaid and draw down federal matching funds. Provider taxes fund approximately $37 billion per year — 18% of states’ total Medicaid financing. Existing taxes are frozen, new taxes are prohibited, and eligibility requirements are tightened. MACPAC and CBO project the restrictions will reduce federal Medicaid spending by an additional $226 billion over the decade, bringing the combined reduction to over $1.1 trillion.[72]

On the workforce side, the OBBBA limits medical students’ access to certain federal loan programs and caps borrowing amounts. This arrives at a moment when rural healthcare is already critically short-staffed and when the same immigration enforcement affecting agricultural and construction labor is reducing the healthcare workforce in the communities that depend most on immigrant providers.[73]

The pattern mirrors agriculture: rising input costs, declining reimbursement, workforce contraction, and policy changes that compound rather than buffer the stress — arriving through independent causal chains, in many of the same rural communities where the farm crisis is most acute. The difference is timing. Agriculture’s cost transmission is already visible in the PPI and beginning to appear in consumer food prices. Healthcare’s cost transmission is masked by the administered pricing structure of the U.S. medical system. The pressure is accumulating in hospital operating margins and provider financials before it surfaces in the CPI healthcare basket or in insurance premiums — which is why the April CPI medical care number understates the forward trajectory in the same way that April food CPI understates the fertilizer cost shock.

Housing

Housing construction exhibits the same margin-squeeze dynamic documented in agriculture — and connects directly to the consumer price data in ways that the headline CPI obscures.

Article 1 established that construction materials trace back to the petrochemical platform: PVC pipe, vinyl siding, insulation foam, adhesives, roofing membranes, and the coatings on structural steel all originate in the same refining and chemical processes now under supply stress. Tariffs have compounded the energy-driven cost increase. Construction input prices surged at a 12.6% annualized rate in the first two months of 2026 — the fastest since early 2022. Since 2020, overall construction input prices have risen more than 43%, with fabricated structural metal products up over 63%.[74]

At the project level, Brookings Institution estimates tariffs alone add $17,500 to the cost of each new home — $30 billion in additional costs across the residential sector. NAHB surveys report tariffs have added roughly $10,000 to homebuilding expenses on top of pre-existing increases. Regulatory costs add an estimated $94,000 per home, approximately one quarter of the final price. The Center for American Progress projects tariff-induced cost increases will result in 450,000 fewer homes built over the next five years, against a deficit that Freddie Mac estimates at 3.7 million units and Brookings at 4.9 million.[75]

Labor is the binding constraint. The industry needs approximately 500,000 additional workers in 2026 to maintain equilibrium, and 94% of contractors report difficulty filling positions. Nearly 40% of skilled construction workers are over 45, with roughly 41% of the current workforce projected to retire by 2031. As documented in the logistics section, immigrants make up 34% of the construction workforce nationally — exceeding 60% in trades like drywall, roofing, and plastering — and 28% of firms report workforce disruptions tied to immigration enforcement in the past six months. Construction wages are up over 4% year-over-year, with specialized trades seeing 9% to 11%.[76]

Builders are responding the way the economics predict. Builder sentiment has spent 21 consecutive months below the breakeven threshold. Forty percent of builders are cutting home prices — the third consecutive month at that level — while absorbing input cost increases they cannot pass through, because buyers cannot pay more. The structural parallel to agriculture is precise: builders, like farmers, are price-takers caught between rising input costs they cannot control and output prices constrained by what the market will bear. Single-family permits fell 15.2% year-over-year in January 2026, with the South — the region building the most housing — down 24.2%. Housing starts hit a five-year low in mid-2025. Multifamily starts are projected at 392,000 units in 2026, declining to 367,000 in 2027.[77]

The units most affected are those most needed. Affordable housing and multifamily construction operate on the thinnest margins and are most sensitive to input cost volatility. A developer facing volatile costs, labor scarcity, and 8–12% target margins makes a rational decision: pause. The projects that get paused are entry-level single-family and multifamily. The projects that proceed are data centers and luxury construction, where margins can absorb the cost structure. The housing units the market most needs are the units the market is least likely to build.

Water scarcity is imposing a second constraint independent of cost. In Arizona, the Department of Water Resources placed a moratorium on new water supply permits, halting approximately 500,000 proposed homes outside Phoenix — some in partially built developments where residents who already moved in are stranded miles from services because planned surrounding construction cannot proceed. In Texas, Hays County attempted a moratorium on water-heavy development but was blocked by state law. Colorado passed a law requiring water districts to provide water to developers who meet land-use requirements, even during drought — while experiencing its worst snowpack on record. The housing shortage and water scarcity are in direct conflict, and states are attempting to address both simultaneously with tools that work against each other.[78]

The April CPI provides the consumer-facing dimension. Shelter — which carries approximately 36% of the CPI basket weight — rose 3.3% year-over-year with a 0.6% monthly gain in April, after months of deceleration. If shelter re-accelerates, it adds roughly one percentage point to headline CPI given its weighting — independent of the energy and food transmission documented elsewhere in this article. The mechanism is straightforward: when new construction contracts, existing housing supply tightens, rents and home prices face upward pressure, and the shelter component of CPI reflects that pressure with a lag of 12 to 18 months. The construction contraction documented above is the leading indicator; the shelter CPI is the trailing one.[24]

Median home prices nationally sit at roughly 5 times median household income, and 8–12 times in coastal metros. Approximately three quarters of American households cannot afford a median-priced new home. That ratio does not improve when new construction contracts, material costs rise, and the available labor force shrinks.

The Aggregate Data and What It Masks

The preceding sections document cost pressure in agriculture, water, healthcare, housing, and logistics — sectors that collectively determine whether households can eat, live somewhere, get medical care, and receive the goods they need. The aggregate economic data does not yet reflect the severity of what those sectors are absorbing. The reason is structural, and understanding it matters for interpreting the numbers that will shape policy, investment, and household decisions over the coming quarters.

GDP composition

The Bureau of Economic Analysis reported 2.0% annualized GDP growth for the first quarter of 2026. Underneath, the composition tells a materially different story. Computer equipment investment surged 67.4%, contributing 0.58 percentage points to growth. Software investment rose 22.6%, contributing another 0.51 points. Combined, those two subcategories — mapping almost entirely to AI and data center buildout — accounted for 1.09 percentage points of a 2.0% total. Bespoke Investment Group calculated that software and IT equipment contributed two-thirds of all GDP growth in the quarter — the largest quarterly technology contribution in history, exceeding the 1999 dot-com peak. Morgan Stanley’s estimate was higher: 75% of GDP growth from AI-related investment.[79]

The economy that feeds and houses people contracted. Residential investment declined. Factory construction fell 22.7%. Consumer spending decelerated. Most non-AI components of business investment were flat to negative. Government spending contributed 0.73 percentage points, buoyed by a federal compensation snapback from the Q4 2025 government shutdown and Iran-related defense outlays. Strip out the AI-driven investment and the government rebound, and private non-tech economic growth was near zero.

A meaningful portion of the capex increase is not building new capacity — it is paying more for the same inputs. Microsoft’s CFO attributed $25 billion of the company’s $190 billion capex to rising memory chip and component costs, not additional infrastructure. DRAM prices more than doubled year-over-year, from $3.76 per gigabyte to $9.71. Meta raised its capex range by $10 billion citing component pricing. The GDP line item “business investment” records this as economic growth — but it is the same phenomenon documented in agriculture and construction: paying more for the same inputs, counted as expansion rather than cost pressure.[80]

The resource competition

The four largest technology companies — Amazon, Microsoft, Alphabet, and Meta — have collectively committed to approximately $725 billion in capital expenditure for 2026, up 77% from the prior year. At roughly 2% of U.S. GDP, that figure is comparable to Singapore’s entire economic output.[81]

That spending does not happen in a separate economy. Data center construction competes for the same finite pool of steel, copper, concrete, diesel, construction labor, water, natural gas, and electrical infrastructure that residential construction, healthcare facilities, water treatment plants, and agricultural operations need. Every construction worker pulled to a data center site at a 9–11% wage premium is a worker not available to build affordable housing or maintain rural hospital facilities. Every ton of steel consumed at 50% tariff pricing is a ton not available for farm equipment or water pipeline construction. The $725 billion is not just masking the squeeze in the headline statistics — it is actively contributing to the squeeze by absorbing inputs the essential sectors documented in this article cannot compete for at the same price points.

The competition operates across multiple resource dimensions simultaneously.

Electricity. Data centers already consume more than 20% of Virginia’s electricity — in the state hosting the world’s largest data center market, approximately 601 facilities including roughly 150 hyperscale centers. In Nevada, NV Energy informed Liberty Utilities — the company serving 49,000 Lake Tahoe residents — that it will stop providing power after May 2027 because it needs the capacity for data centers. Data centers used 22% of Nevada’s electricity in 2024; NV Energy’s own resource plan projects that could reach 35% by 2030, with approximately 75% of major-project load growth attributed to data centers concentrated in Northern Nevada. Liberty gets 75% of its power from NV Energy, and California regulators — who oversee Liberty — have no jurisdiction to compel Nevada to maintain the supply. Lake Tahoe residents report electricity prices up approximately 77% since late 2022.[82] EIA data shows average revenue per kilowatt-hour up 9% nationally in February 2026, with the sharpest increases in data-center-heavy states: Virginia 26.3%, Ohio 21.9%, Pennsylvania 19.5%.[83]

Water. A single large data center can consume up to 2.7 million gallons of water per day during peak summer cooling, with roughly 80% lost to evaporation. Over 90% of U.S. data centers draw cooling water directly from the municipal systems serving surrounding residents and farms. Two-thirds of new hyperscale campuses built since 2022 are sited in counties classified as high water stress.[84] In the Texas Panhandle, four data centers are planned in communities sitting over the Ogallala Aquifer — the groundwater system supporting one-fifth of national wheat, corn, cotton, and cattle production. The Ogallala has lost 30% of its supply. Texas does not require most data centers to report their water usage.[85] Virginia is experiencing its second-driest recharge season since records began in 1895, with virtually the entire state in drought — while hosting the world’s highest concentration of data centers.[86]

Natural gas. The scale of electricity demand from data center construction has outgrown what the existing grid can deliver in many locations. The response has been to build on-site natural gas-fired power plants, bypassing the grid entirely and becoming direct industrial consumers of the same constrained supply that feeds fertilizer production, powers helium extraction, fuels petrochemical manufacturing, and generates residential electricity. In the Permian Basin, a single planned complex — GW Ranch in Pecos County — is approved for 7.65 gigawatts of gas-fired power. At full capacity, a Baker Institute energy economist calculated it could consume 4 to 7% of all natural gas produced in the Permian Basin. In Memphis, a data center operator installed 35 gas turbines on a natural gas main, generating 422 megawatts, with 41 additional turbines recently approved in Mississippi for 1.2 gigawatts. The turbines were installed without environmental permits, classified as “portable” to sidestep review.[87]

Labor. The same sector driving the capex surge is simultaneously cutting workers at the fastest pace in years — more than 85,000 tech job cuts in the first four months of 2026, up 33% year-over-year, with AI cited as the leading reason. The workers being eliminated — customer support, quality assurance, middle management — are different people than the workers being hired: machine learning engineers commanding 56% wage premiums, with 275,000 AI-related positions posted simultaneously. Aggregate unemployment remains low while the labor market restructures underneath the headline number — the same masking dynamic observed in the GDP composition.[88]

More than 1,500 new data centers are in development nationwide, with the majority planned for rural areas — particularly across the South (754 planned facilities) and Midwest — the same regions where the farm bankruptcy and input cost crises documented earlier in this article are most severe. Data centers are sited in these areas because they offer cheap land, natural gas pipeline access, and economic incentives.[89] The geographic overlap with the agricultural crisis is not coincidental. It means the resource competition is most intense precisely where the existing sectors are most financially stressed.

The competition is producing pushback — at least $85 billion in data center projects have faced cancellation or significant community resistance since 2023, and the pace is accelerating. The evidence for that self-correction, and what it means for the trajectory documented in this article, is examined in the final section.

What the aggregate numbers measure

The CPI and PPI data from “Where the Data Stands” measure the same tension from a different angle. CPI at 3.8% tells you consumer prices are rising. PPI at 6.0% tells you the pressure behind those prices is larger than what’s reached consumers. The 220 basis point gap tells you the lag is real and the direction is up. Core CPI at 2.8% with core PPI at 5.2% tells you the broadening is not just energy. The PPI trade services margin surge — 2.7% in a single month, the largest on record — tells you tariff costs are beginning to pass through the wholesale and retail chain.

The conditions described across these sectors — supply-driven inflation through energy, materials, logistics, and input costs, arriving concurrently with economic deceleration in agriculture, construction, and consumer-facing sectors — have historically been associated with stagflation: persistent inflation driven by supply constraints rather than excess demand, combined with stagnating or declining economic activity in key sectors of the real economy.

Whether the United States is in or will enter a period of stagflation depends on how the aggregate statistics settle out over the coming quarters. GDP may remain technically positive. Unemployment may remain low in aggregate. But the headline numbers are already masking the sectoral reality — as the Q1 GDP composition demonstrates. The Federal Reserve faces the textbook stagflationary dilemma: raising rates worsens the economic deceleration, lowering rates worsens the inflation.

Whether or not the precise definition is met in the aggregate data, the lived experience for households exposed to food costs, housing costs, healthcare costs, and energy costs may begin to resemble the conditions. Prices rising while economic prospects diminish — not because demand is too strong, but because supply is too constrained, too expensive, and too concentrated to serve every sector at once.

The final article in this series examines what this economic environment has historically meant for financial assets and savings — and why the standard playbook may not apply in the ways investors expect.

The Future Is Not Written

I am a financial advisor, not an economist, agricultural policy expert, or water systems engineer. The connections documented above are sourced, but I do not know what I do not know. What follows is an honest accounting of what is working against the trajectory the data suggests. The counterarguments operate on different timelines — some provide meaningful buffer in the next twelve to eighteen months, others are building toward a different system in the two-to-three year range — and that distinction matters.

Near-term buffers

The Mississippi River, like western snowpack, is subject to weather variability that cuts in both directions. This article documents four consecutive years of low water. Most of the water in the Lower Mississippi comes from upstream tributaries — the Ohio, Missouri, and Tennessee Rivers — rather than local rainfall. A wet year across the Midwest and Ohio River Basin would improve river levels the same way a good snow year improves Colorado River storage. An Army Corps of Engineers official noted that the pattern is cyclical and that the recent dry trend was preceded by a lengthy wet period that did not end until 2020. Four consecutive dry years is a deeper deficit than one season of rain typically fills, and planning around favorable weather is not a strategy. But the trajectory is not locked in — the river has recovered before.[90][91]

The food surplus and waste reduction buffers documented in the first article remain real. The United States produces substantially more food than it consumes domestically, and Americans waste roughly 70 million tons of food per year — waste that declined by 25% during the pandemic through behavioral change alone. These buffers do not prevent price increases, but they provide meaningful margin before the disruption reaches the level of genuine food scarcity. The pain arrives as higher grocery bills before it arrives as empty shelves.

The dairy market illustrates how agricultural systems adapt under stress, even when the adaptation itself creates new pressures. The U.S. dairy herd expanded to 9.62 million head by February 2026 — the largest since 1993 — while global milk production surged approximately 5.5% in late 2025, nearly four times the long-run average. The expansion was driven by strong margins in 2024, lower feed costs, accumulated improvements in genetics and management, and roughly $10 billion in new processing capacity added between 2023 and 2026. The result is an oversupply severe enough to push wholesale dairy prices well below cost of production — Class IV futures fell from $22–23 to the $13 range — even as feed, diesel, and electricity costs rise.[92]

The dairy glut is occurring alongside its mirror image in beef. The beef cattle herd has contracted to its smallest size since 1951, supporting the 2.7% monthly beef price increase documented in the April CPI. The two markets are connected by the same genetics technology: sexed semen allows dairy farmers to guarantee female replacement heifers while breeding surplus cows to beef bulls, creating “beef-on-dairy” crosses as a revenue stream. That technology incentivized dairy herd expansion — which contributed to the oversupply — while simultaneously providing a partial supply bridge into the beef deficit.[93]

The system is responding. USDA has proposed diverting 800,000 to 1,000,000 dairy-origin cattle into the beef supply to address both the dairy oversupply and beef shortage simultaneously. The corn-to-soybean acreage shift documented in the farm section — driven by soybeans’ lower fertilizer requirements — is itself a real-time adaptation to the nitrogen cost spike. Farmers are not static. They adjust crop mix, input strategies, and marketing plans in response to changing economics. Those adjustments are imperfect and often insufficient to close the margin gap, but they are measurable and they are happening.[94]

The USMCA review scheduled for July introduces uncertainty. More than 40% of U.S. dairy export value — $2.58 billion from Mexico and $1.31 billion from Canada — flows to North American neighbors. If that trade is disrupted, the oversupply has fewer outlets. But the review is also an opportunity: dairy market access has been a persistent U.S. trade objective, and the current oversupply strengthens the negotiating case for expanded export access.[95]

Structural adaptation

As documented in the first article, the European Union’s response to losing 45% of its natural gas imports after Russia’s invasion of Ukraine demonstrates that crisis-driven adaptation can outpace expert predictions. Germany built its first LNG terminal in nine months. European gas consumption fell more than 18% in two years. The predicted catastrophe did not materialize. The adaptation was primarily behavioral and policy-driven — demand reduction, emergency permitting, legislative response — domains where urgency and political will can compress timelines in ways physical infrastructure cannot. The current disruption is more severe in important ways — there is less slack and fewer alternative sources — but the pattern of adaptation exceeding expectations is documented and real.

The data center buildout that is masking sectoral contraction in headline GDP — and competing for the water, natural gas, electricity, and labor that essential sectors need — is simultaneously being constrained by the communities it affects. Heatmap News reported that at least $85 billion in data center projects have been canceled over the past three years due to local opposition, with the pace accelerating: two cancellations in 2023, six in 2024, twenty-five in 2025, and twenty in the first quarter of 2026 alone.[96] Communities in at least 14 states have enacted temporary pauses on data center development, and 36 states are now considering new rules around data center water use. In Utah, a major developer withdrew a water application after 3,900 public protests — then announced plans to refile, illustrating both the strength and the limits of community opposition.[97] The American Farm Bureau Federation issued a formal policy statement — “Balancing Data Center Growth” — objecting to data center electricity demand driving up rates for agricultural operations.[98] The federal AI executive order of December 2025 explicitly does not preempt state permitting, zoning, or energy regulations, and governors in California, Colorado, and New York have stated the order will not prevent enforcement of local rules.[99]

Every data center that does not get built returns steel, copper, water, electricity, and labor to the pool available for housing, healthcare, and agricultural infrastructure. The self-correction is slow and contentious, but it is measurable — and it means the $725 billion in committed hyperscaler capex will not all be spent, which both reduces the GDP masking effect and relieves pressure on the competing sectors documented throughout this article.

Supply chains are restructuring. Companies are diversifying suppliers, regionalizing sourcing, and building redundancy into systems optimized for efficiency at the expense of resilience. The shift from “just-in-time” to “just-in-case” was already underway; the Hormuz closure accelerated it. CHIPS Act semiconductor fabs are transitioning from funding announcements to production ramp-ups, structurally reducing the concentration risk this series has documented. Every dependency exposed by this crisis — single-source helium, grade-specific crude, concentrated fertilizer trade routes — is a vulnerability that companies and governments are now actively working to reduce because the theoretical risk became a real cost.[100][101] The pharmaceutical supply chain is following the same pattern: Lupin announced a $250 million investment in a U.S. production facility in Florida; the European Union reached a provisional agreement on the Critical Medicines Act on May 12, 2026, establishing mandatory shortage prevention plans, supply chain diversification requirements, and a Union list of critical medicinal products with vulnerability assessments — the most significant pharmaceutical supply chain legislation in the EU’s history, produced directly by the crisis this series documents.[102]

The helium supply map is being redrawn. Saskatchewan is producing helium independently of natural gas. Tanzania is targeting production in 2027. Six new U.S. operations came online in 2025 alone. The crisis price signal has made previously uneconomical exploration viable across multiple continents. Five years from now, helium supply will be more geographically diversified than at any point in the industry’s history — a permanent structural improvement produced directly by this crisis.

Energy transition is being accelerated, not killed. Every dollar of elevated gasoline price strengthens the economic case for hybrids and electric vehicles. Every natural gas price spike makes solar and wind more competitive for electricity generation. Every fertilizer shortage strengthens the case for precision agriculture that uses less input per acre. But the economic case and the deployment case are not the same thing. Energy infrastructure requires capital commitments on 10- to 20-year horizons, and U.S. energy policy has reversed direction with every change of administration for more than two decades — a cycle that undermines the investment certainty large-scale projects require. The crisis does not solve the transition — the timeline is measured in decades, not years — and the path from stronger economic incentive to actual energy system change depends on policy stability that does not currently exist. But the economic signal just got materially stronger, and that signal is permanent in a way that policy is not.

Agricultural crises have historically produced systemic improvements, even when the transition is brutal for the people living through them. The 1980s farm crisis — to which the current situation is most often compared — devastated individual operations but also produced the modern farm safety net, drove consolidation toward more efficient operations, and ultimately resulted in a more productive agricultural system.

Water infrastructure investment, while decades late, is being forced by the crisis. Corpus Christi’s reversal on desalination, the Colorado River negotiations, the data center water fights — all are compelling investment in desalination, water recycling, and aquifer recharge that was deferred during decades of assumed abundance. The investment arrives because the alternative is running out of water.

The range

None of this helps the farmer who goes bankrupt this year, the hospital that cannot source helium this month, or the household putting groceries on a credit card this week. The pain is real, it is regressive, and it falls hardest on those with the least margin. But crises produce adaptation. The system that emerges on the other side is typically more resilient than the one that entered — because the vulnerabilities that were invisible during stable times get exposed and addressed under stress.

The future is not written. The range of outcomes is wide. Readers should plan for the range, not for either endpoint.

Notes

[1] BLS, “Consumer Price Index — April 2026,” USDL-26-0721, May 12, 2026. All CPI figures from this release. Link

[2] BLS, “Producer Price Indexes — April 2026,” USDL-26-0723, May 13, 2026. All PPI figures from this release. Link

[3] BLS CPI release for energy sub-components. EIA electricity revenue data from EIA “Electric Power Monthly,” reported in Utility Dive, April 2026.

[4] BLS CPI release for food sub-components.

[5] USDA milk production data; global oversupply documented in StoneX/Nate Donnay analysis and FCS America/Terrain dairy outlook Full dairy-beef dynamic (herd inversion, genetics cycle, margin compression, proposed USDA rebalancing program) reserved for “The Future Is Not Written” section.

[6] Same BLS PPI release. Trade services +2.7%, truck freight +8.1%, Stage 1 intermediate demand +8.9% YoY, services +1.2% MoM.

[7] CBS Los Angeles, May 5, 2026; ABC7 Los Angeles, May 4, 2026.

[8] EIA May 2026 Short-Term Energy Outlook.

[9] Morgan Stanley analyst note, May 4, 2026. Global drawdown of 4.8 million bpd cited via Fortuneand Bloomberg US distillate stockpiles lowest since 2005 per EIA data cited in same. (Morgan Stanley research via

[10] Same Morgan Stanley note. 222 million barrels as of late April per EIA; base case projection below 200 million by end of August; collapse in East Coast imports; refinery slate shift. Reported via Reuters, Bloomberg, Seeking Alpha.

[11] IEA-coordinated strategic reserve release of 400 million barrels. Reported via Fortune

[12] AP reporting on helium containers stranded. Replaces OilPrice.com.

[13] SEMI chief of staff Bettina Weiss via Foreign Policy, April 27, 2026.

[14] S&P Global Platts reporting on Saudi OSP, April 2026. Arab Light premium of $19.50 over benchmark. Dated Brent at $132-$144 vs futures at $96-$100 per CNBC reporting (Pavel Molchanov, Raymond James).

[15] American Farm Bureau Federation, “Farm Bankruptcies Continued to Climb in 2025,” February 9, 2026. Acceptable — AFBF is the standard source for this data. Link

[16] AFBF, February 2026, citing USDA data.

[17] USDA Economic Research Service, “Farm Sector Income & Finances: Farm Sector Income Forecast,” February 5, 2026. Link

[18] Purdue Center for Commercial Agriculture survey, March 2026. Reported via PBS News.

[19] farmdoc dailyand Iowa State University Extension. CME Group market data.

[20] NDSU Agricultural Risk Policy Center, presented at Federal Reserve Bank conference. Reported via Investigate Midwest.